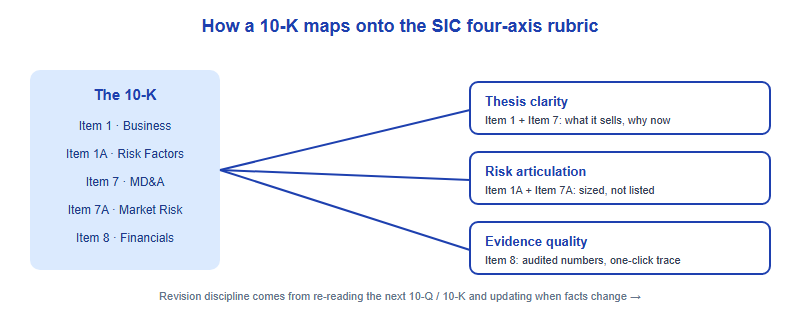

To read a 10-K efficiently for the Student Investment Challenge (SIC), do not read it front to back. Go straight to four places: Item 1 (Business) for what the company actually sells, Item 1A (Risk Factors) for the company's own list of what could break the thesis, Item 7 (MD&A) for management's explanation of the numbers, and Item 8 (Financial Statements) for the audited figures you will cite. Everything else is context. This guide shows what to pull from each so it maps onto SIC's four-axis rubric.

Why the 10-K is the document SIC actually rewards

A Form 10-K is the comprehensive annual filing that U.S. publicly reporting companies must submit to the Securities and Exchange Commission (SEC) under federal securities law. It is filed once a year and contains audited financial statements — which is precisely what makes it different from the glossy "annual report to shareholders" full of photography and CEO letters. You find 10-Ks for free in the SEC's EDGAR database, searchable by company name with a filter for the "10-K" filing type.

This matters for SIC because of how the program scores you. SIC — the China and Asia editorial desk operated by Hanlin Education, a five-month academic research program running roughly March to August, not the Wharton Global Youth High School Investment Competition, which is a separate, ranked, portfolio-performance contest — judges work on a four-axis rubric: thesis clarity, evidence quality, risk articulation, and revision discipline. The published rubric is blunt about sourcing. It demands "primary sources — 10-Ks, earnings transcripts, Fed minutes," not blog summaries or "as reported by." And it sets a test: every cited number must trace back to a document a judge can open in one click, and "if we cannot reach the underlying source in 30 seconds, the citation is decorative. Decorative citations score zero." The 10-K is the single document that lets you satisfy that standard for almost any equity thesis. (For the full picture, see What Is the SIC and the SIC rubric breakdown.)

The map: which items matter, and what to extract

A 10-K is organised into numbered "Items" grouped under four Parts. You do not need all of them. The table below lists the high-value items, their exact SEC titles, what they contain, and the one thing to extract for an SIC thesis. Skim the rest.

| Item (exact SEC title) | What it contains | Extract this for SIC | Priority |

|---|---|---|---|

| Item 1 — Business | Description of the business: main products and services, subsidiaries, and the markets it operates in. | One sentence on how the company makes money. If you cannot write it, you do not have a thesis yet. | High |

| Item 1A — Risk Factors | The most significant risks that apply to the company or its securities, in the company's own words. | The 2–3 risks that would actually break your thesis — for Risk Articulation. | High |

| Item 3 — Legal Proceedings | Significant pending lawsuits or legal proceedings beyond ordinary litigation. | Any litigation large enough to move the numbers; note it as a risk. | Medium |

| Item 5 — Market for Registrant's Common Equity… | Equity securities, shareholder data, dividends, and share repurchase activity. | Buybacks and dividends — capital-return signals that support or undercut a thesis. | Medium |

| Item 7 — Management's Discussion and Analysis (MD&A) | Management's perspective on results: operations, liquidity, capital resources, critical accounting judgments. | The "why" behind revenue and margin changes — and the language to quote precisely. | Highest |

| Item 7A — Quantitative and Qualitative Disclosures About Market Risk | Exposure to interest-rate, foreign-currency, commodity-price, or equity-price risk. | Macro sensitivities (rates, FX) to size in your risk section. | Medium |

| Item 8 — Financial Statements and Supplementary Data | Audited income statement, balance sheet, cash-flow statement, statement of stockholders' equity, plus the notes. | Every number you cite. The notes are where the real story often hides. | Highest |

Two practical notes. First, the notes to the financial statements (inside Item 8) are not optional. Revenue recognition policy, segment breakdowns, debt maturities, and stock-based compensation all live there, and they frequently change how a headline number should be read. Second, read MD&A (Item 7) before the statements, not after. Management tells you which lines moved and why; you then verify their explanation against Item 8 rather than starting from a wall of numbers.

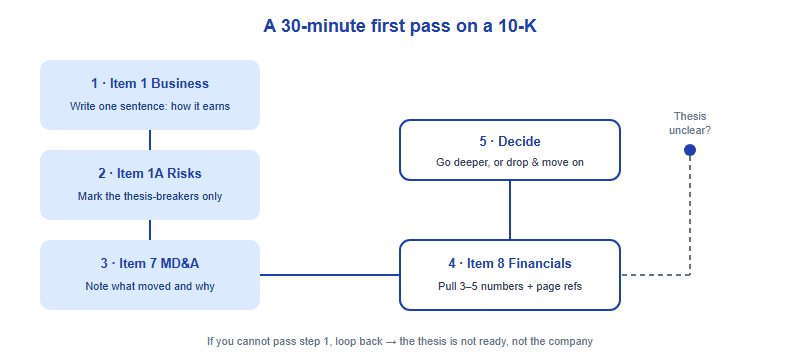

A 30-minute first pass that produces citable material

You will not read a 200-page filing in one sitting, and you should not try. The goal of a first pass is to decide whether the company is worth a full thesis and to capture a handful of numbers you can defend. Here is a sequence that respects the SIC "one-click trace" standard from the start.

- Item 1 (≈5 min): Read enough to write a single plain sentence on how the company makes money. If you can't, that's your signal — keep reading until you can, or move to a simpler company.

- Item 1A (≈8 min): Skim the risk headings. Ignore boilerplate ("general economic conditions"). Mark only the 2–3 risks that would specifically invalidate the thesis you're forming.

- Item 7 / MD&A (≈10 min): Find management's explanation of revenue and margin movement. Copy the exact phrasing of any claim you might rely on, with the page number.

- Item 8 (≈7 min): Pull three to five numbers — revenue, operating margin, free cash flow, net debt, whatever your thesis turns on — each with the statement and page reference so it survives the 30-second click test.

By the end you have a one-sentence thesis, a short risk list, and a handful of traceable figures. That is the raw material the rubric's Evidence Quality and Thesis Clarity axes reward — and it took half an hour, not a weekend.

Turning 10-K extracts into rubric points

Reading the filing is half the job; the other half is converting what you found into the four things SIC scores. The mapping is direct, and it is the part most students skip.

| SIC rubric axis | What the judge is checking | 10-K source & move |

|---|---|---|

| Thesis clarity | Can a non-expert grasp the thesis in two sentences? | Compress Item 1 (the business) + the key MD&A driver into one claim a classmate understands. |

| Evidence quality | Does each number trace to a primary source in one click? | Cite Item 8 figures with the statement name and page; link to the EDGAR filing, never a third-party summary. |

| Risk articulation | Are risks identified and sized, not just listed? | Take 2–3 Item 1A / Item 7A risks and quantify the hit to your numbers if each materialised. |

| Revision discipline | Did the thesis update when facts changed? | Re-read the next 10-Q or 10-K; if a driver or risk shifted, revise and document the change. |

The risk row is where strong entries separate from average ones. The rubric explicitly rewards risk that is sized, not merely named. "Customer concentration is a risk" is a list item. "Their top customer was 38% of revenue per the segment note, so losing it cuts revenue by roughly a third" is articulation — and the 38% came straight from the notes inside Item 8. Same source, completely different score.

One discipline that pays off across every axis: quote the company against itself. When MD&A says growth was "driven primarily by pricing," that is a testable claim — check whether unit volumes actually fell. SIC's judges value reasoning that engages the primary document, not reasoning that decorates a conclusion with a citation. For where this sits in the wider program design and how it differs from a ranked, performance-based contest, see SIC vs the Wharton Global HS Investment Competition.

Common mistakes that cost rubric points

- Reading the annual report instead of the 10-K. The shareholder annual report is a marketing document; the 10-K is the audited filing. Cite the 10-K.

- Citing "as reported by" secondary sources. The rubric scores blog and Reddit summaries as zero. Go to EDGAR and cite the filing directly.

- Listing risks without sizing them. Item 1A gives you the company's risk list; your job is to estimate the impact, not reproduce the list.

- Skipping the notes. Segment data, revenue recognition, and debt maturities live in the Item 8 notes and routinely reverse a naïve reading of the headline numbers.

- Treating the 10-K as a one-time read. Revision discipline is an explicit axis. Re-checking later filings and updating your thesis is rewarded behaviour, not wasted effort.

FAQ

Where do I find a company's 10-K for free?

In the SEC's EDGAR database at sec.gov, searchable by company name with a "10-K" filing-type filter. It is free and is the primary source SIC's rubric expects.

Is a 10-K the same as an annual report?

No. The 10-K is the audited filing required by the SEC. The "annual report to shareholders" is a separate, often glossy document. For SIC, cite the 10-K.

Which 10-K section matters most for an SIC thesis?

Item 7 (MD&A) for the "why" and Item 8 (financial statements) for the audited numbers. Item 1A (Risk Factors) drives your risk section.

Do I have to read the whole 10-K?

No. Run a focused first pass — Items 1, 1A, 7, and 8 — to extract a thesis, sized risks, and traceable numbers. Confirm current SIC requirements on the official SIC site.

Talk to an advisor · message us directly:

- 💬 WhatsApp — message an advisor directly → · fastest reply

- 📧 Email meiqiqiang@linstitute.net · 24h reply

Published by the SIC editorial desk, operated by Hanlin Education for China-based international-school students. Official rules are set by the competition and change yearly, so confirm current details (registration, deadlines, eligibility, format) on the official SIC / organiser site. SIC is distinct from the Wharton Global Youth High School Investment Competition, which is a separate program. Confirmed errors are corrected within 7 working days.