Building a strong Student Investment Challenge (SIC) portfolio means choosing a small set of holdings, sizing each by how much evidence you actually have, spreading risk so one wrong call cannot sink the case, and writing a single narrative that ties every position back to one defended thesis. SIC judges score the reasoning behind your portfolio — thesis clarity, evidence, risk, and revision — not your terminal return, so construction is an argument, not a bet.

Construction follows the rubric, not the ticker tape

Before you pick a single stock, internalise the one rule that governs every SIC decision: on the official site, “advancement turns on the clarity and articulation of the thesis, not on the growth of the portfolio.” That sentence should change how you build. A portfolio that gained 20% on a lucky meme stock with no written reasoning scores worse than a flat portfolio where every holding is sized, justified, and revised on the record.

SIC runs two tracks. The Junior Division is an individual entry running a simulated portfolio with a weekly thesis log; the Senior Division is a team of 2–4 producing an investment strategy report. Both are judged on the same four-axis rubric — Thesis Clarity, Evidence Quality, Risk Articulation, and Revision Discipline — so the way you build and document a portfolio has to feed all four axes. If you are new to the program, start with our explainer on what the SIC actually is, then come back here to build.

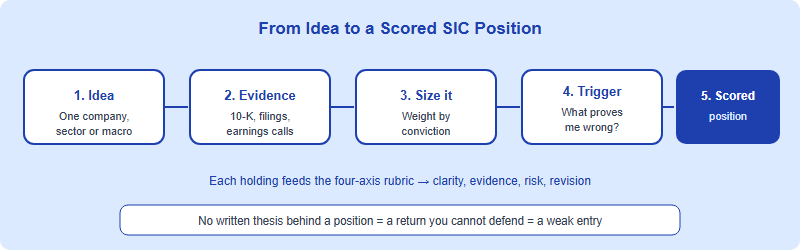

The practical consequence: every position in your portfolio is a claim you will have to defend. So the first construction question is never “what will go up?” It is “what can I argue, with primary sources, and what would prove me wrong?” The diagram below shows how a single holding flows from idea to a scored, rubric-aligned position.

Position sizing: let conviction, not excitement, set the weight

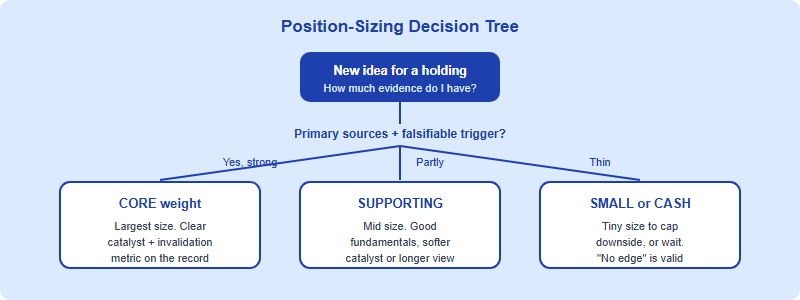

Position sizing is the single most revealing construction decision you make, because a weight is a number that exposes how much evidence you actually have. A 30% position says “I have strong, primary-source conviction and a clear catalyst.” A 5% position says “interesting idea, thinner evidence, I am keeping the downside small.” When your sizing and your written conviction disagree — a huge bet behind a one-line, news-sourced thesis — judges notice immediately, and it costs you on both Thesis Clarity and Risk Articulation.

The official SIC site does not publish position limits, a maximum number of holdings, a minimum diversification rule, or the amount of virtual capital — these scale by division and can change by season, so confirm current parameters on the official site rather than assuming a number. What is durable across seasons is the principle: size to the strength of your argument, and never let a single position be large enough that being wrong erases your ability to make a clear case. The first-party “conviction tier” framework below is how our editorial desk teaches Chinese international-school students to translate evidence into a weight.

| Conviction tier | Evidence you must have | Indicative weight* | Rubric axis it strengthens |

|---|---|---|---|

| Core (high) | Primary sources (10-K, filings, earnings calls), a specific catalyst, and a falsifiable failure metric | Largest single weights | Thesis Clarity + Evidence Quality |

| Supporting (medium) | Solid fundamentals but a softer catalyst or a longer time horizon | Mid-sized weights | Risk Articulation |

| Exploratory (low) | Plausible idea, thinner evidence, kept deliberately small to cap downside | Smallest weights | Revision Discipline (you can scale up later if facts confirm) |

| Cash / unallocated | “No edge yet” is a legitimate, defensible stance | Whatever you cannot justify | Risk Articulation (discipline to wait) |

*Indicative only. SIC publishes no fixed position limits; actual weights and any caps scale by division and season — confirm on the official site.

Notice the bottom row. Holding cash because you have not yet built an argument is not laziness — it is exactly the “discipline to wait” that the rubric rewards under Risk Articulation. A portfolio fully invested in ideas you cannot defend is weaker than a partly invested one where every dollar has a written reason.

Diversification: spread the reasons, not just the tickers

Beginners diversify by buying ten stocks. SIC-grade diversification is subtler: you spread your risk factors so that no single assumption can break the whole portfolio at once. Six holdings that are all bets on falling interest rates are not diversified — they are one trade wearing six tickers. If rates surprise to the upside, every position fails together, and your “revision” looks like panic rather than discipline.

The test is to ask, for your collection of holdings: what single event would damage the most positions simultaneously? If the answer is “one macro surprise,” your real diversification is low regardless of how many names you hold. Map your portfolio against a few independent risk drivers — interest-rate sensitivity, sector cyclicality, geographic exposure, company size, and growth-versus-value style — and check that you are not stacked on one side of any of them. This kind of structured risk thinking is also what separates SIC’s evaluation philosophy from a pure trading contest; see our breakdown of SIC vs the Wharton Global Youth investment competition (a different organisation with a tournament, ranked format) for why the judging logic differs.

Portfolio-level risk: name the failure before it happens

Risk Articulation is one of the four equally weighted rubric axes, and the official guidance is concrete: state what would invalidate your thesis using falsifiable metrics, not generic worry. The published example sets the bar — something like “gross margin below 38% in two consecutive quarters,” not “the company might face competition.” That standard applies at the portfolio level too: for each material holding, write the specific number, threshold, or event that would tell you the thesis has failed.

Three portfolio-risk habits that earn points:

- Per-position invalidation triggers. Every core and supporting holding gets one falsifiable line: the metric and the timeframe that would force you to cut or revise it.

- A correlation check. Identify the one macro or sector event that would hit the most positions at once, and decide on purpose whether you are comfortable carrying that concentration.

- Sizing discipline. Make sure no single position is so large that being wrong about it destroys your ability to present a coherent case — concentration is fine when it is justified and bounded, reckless when it is neither.

The most common reason strong portfolios lose risk points is the opposite of carelessness: students quietly rewrite a losing thesis to match the price, instead of admitting the trigger fired and revising on the record. The rubric calls this out directly under Revision Discipline — “quietly mutating” a thesis to justify returns scores worse than an honest, documented change of mind.

Conviction and the narrative: tie every holding to one thesis

Here is the construction step beginners skip: a SIC portfolio is not a list of independent ideas — it is one argument expressed through several positions. The narrative is the sentence (or short paragraph) that explains why these holdings belong together. “I believe X, so I am overweight A and B, hedged by C, and avoiding D” is a portfolio with a spine. Six unrelated stock picks, however good individually, read as six theses competing for the reader’s attention and dilute your Thesis Clarity score.

Conviction is what links sizing to narrative. Your largest positions should be the cleanest expressions of your central view; your smallest should be hedges, optionality, or genuinely separate bets you are keeping contained. When a judge reads your weights top to bottom, the story should be obvious without you explaining it. Use this template to pressure-test the whole book:

| Narrative element | One-sentence test | If you cannot answer… |

|---|---|---|

| Central thesis | Can a non-expert understand my core view in two sentences? | Your Thesis Clarity is at risk — simplify before you size. |

| Why these holdings | Does each position express the central view or deliberately offset it? | You may be holding noise — cut it or justify it explicitly. |

| Why these weights | Do my biggest positions match my strongest evidence? | Re-size: a big bet on thin evidence is the classic deduction. |

| What breaks it | Can I name the event that damages most positions together? | Your diversification is weaker than your ticker count suggests. |

| What changed | Did I revise on the record when a trigger fired? | Revision Discipline points are slipping — log the change honestly. |

For the Junior Division, this narrative lives in your weekly thesis log; for the Senior Division, it becomes the connective tissue of the 15–30 page strategy report (page counts and review-round details scale by season — confirm on the official site). Either way, the discipline is the same: write the thesis first, size to it, and let the portfolio be the argument. If you want the underlying scoring logic in detail, our walkthrough of the SIC four-axis rubric shows exactly what each axis rewards.

A simple build order you can reuse every season

- 1. Write the central thesis first — one or two sentences a non-expert understands.

- 2. Source the evidence — primary documents only; if a reader cannot reach the source fast, it scores as decorative.

- 3. Assign conviction tiers — core / supporting / exploratory / cash, per the table above.

- 4. Size to conviction — biggest weights on strongest evidence; cap any single bet so being wrong is survivable.

- 5. Spread the risk factors — check no single event breaks most positions at once.

- 6. Write per-position triggers — falsifiable metric + timeframe for each material holding.

- 7. Log revisions honestly — when a trigger fires, change the thesis on the record, not retroactively.

Do these seven in order and your portfolio will read the way SIC judges want: a clear view, defended with evidence, with risk named in advance and revisions made in the open. That is construction as argument — and it is what advancement turns on.

Frequently asked questions

How many stocks should a SIC portfolio hold?

The official site sets no required number. Hold as many as you can defend with primary evidence and distinct reasons — quality of argument beats raw count.

Does a higher portfolio return help me advance in SIC?

No. The official rule is that advancement turns on thesis clarity and reasoning, not portfolio growth. Returns alone do not earn rubric points.

How big can one position be?

SIC publishes no fixed position cap; limits scale by division and season — confirm on the official site. The durable principle: size to evidence and keep any single bet survivable.

Is holding cash allowed and does it hurt my score?

Holding cash when you have no defensible edge is legitimate and can strengthen your Risk Articulation. Discipline to wait beats forcing weak positions.

Talk to an advisor · message us directly about building and defending your SIC portfolio:

- 💬 WhatsApp — message an advisor directly → · fastest reply

- 📧 Email meiqiqiang@linstitute.net · 24h reply

Published by the SIC editorial desk, operated by Hanlin Education for China-based international-school students. Official rules — divisions, deliverables, position parameters, dates, and recognition tiers — are set by the competition and change yearly, so confirm current details on the official SIC / organiser site before you rely on them. This site is independent editorial guidance and is distinct from the Wharton Global Youth High School Investment Competition. Confirmed errors are corrected within 7 working days.