For the Student Investment Challenge (SIC), valuation is how you turn “I like this company” into “this stock is mispriced, and here is the number.” Two tools cover almost everything a beginner needs: comparable multiples (fast, market-based) and a simple discounted cash flow, or DCF (slower, assumption-driven). This guide explains when to use each, how to keep your work defensible, and the valuation mistakes SIC judges spot first.

Why valuation matters in SIC (and what judges actually reward)

SIC is a CEE-endorsed competition for students in grades 6–12, and its evaluation principle is blunt: “advancement turns on the clarity and articulation of the thesis, not on the growth of the portfolio.” That single line should shape how you value a stock. The point of a valuation is not a precise price target to two decimals — it is a defensible argument that the market price and the company’s fundamentals disagree, and that you can say why.

Whether you are in the Junior Division (Trading Track) writing weekly thesis logs or the Senior Division (Strategy Track) building a team strategy report, the same skill applies: pick a method, state your assumptions, and show your work. A simple valuation you can defend beats an elaborate one you cannot. If you are still mapping out the whole season, our complete SIC 2026 guide covers the format and timeline; this article zooms in on the valuation toolkit itself.

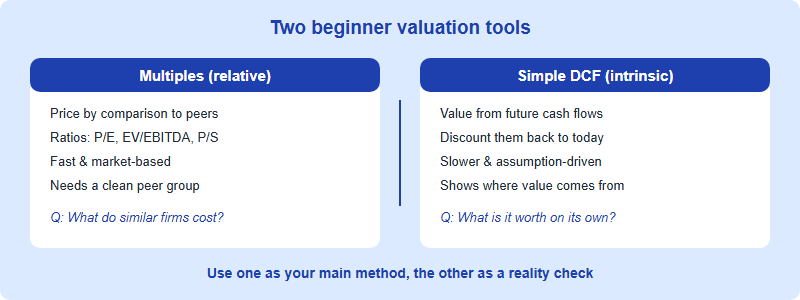

The two tools: multiples vs a simple DCF

Almost every beginner valuation reduces to two approaches. Relative valuation (multiples) prices a company by comparison: if similar firms trade at a certain ratio, this one probably should too. Intrinsic valuation (DCF) prices a company from the inside: it estimates future cash flows and discounts them back to today. They answer slightly different questions, and strong pitches usually use one as the main argument and the other as a sanity check.

Multiples in one minute

A multiple is just a ratio of price to a fundamental. The two most common are P/E (price per share ÷ earnings per share) and EV/EBITDA (enterprise value ÷ earnings before interest, taxes, depreciation and amortisation). You find a peer group of similar companies, take their median multiple, and apply it to your company’s earnings or EBITDA to get an implied value. One rule beginners often miss: keep the numerator and denominator apples-to-apples. Enterprise value (EV) belongs to all investors, so it pairs with EBITDA; equity value (market cap) belongs only to shareholders, so it pairs with net income. Mixing them — for example EV ÷ net income — produces a meaningless number that a sharp judge will flag immediately.

A simple DCF in one minute

A DCF says a company is worth the cash it will generate in the future, adjusted for the fact that money later is worth less than money now. For a beginner, three inputs drive everything: a few years of projected free cash flow, a discount rate (how risky those cash flows are), and a terminal value (everything beyond your forecast). You do not need a 200-row spreadsheet. A clean 5-year forecast with stated assumptions is more persuasive in SIC than a complex model whose inputs you cannot explain when a judge asks “why 12%?”

The DCF’s strength is also its danger: because every output flows from your assumptions, small changes compound. Nudging the growth rate up by two points or the discount rate down by one can swing the value by a quarter or more. That sensitivity is not a flaw to hide — it is precisely why stating assumptions and showing a range, covered below, separates a credible SIC pitch from a flattering one.

| Dimension | Multiples | Simple DCF |

| Speed | Fast — minutes once you have peers | Slower — needs forecasts |

| Main inputs | Peer ratios + your company’s earnings/EBITDA | Cash-flow forecast, discount rate, terminal value |

| Biggest strength | Anchored to real market prices | Shows where value comes from |

| Biggest weakness | Garbage peer group → garbage answer | Tiny assumption changes swing the result |

| Best use in SIC | Fast read; cross-check on a DCF | Core argument when you have a clear view |

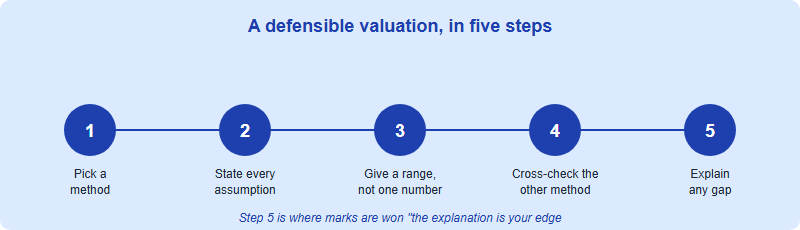

How to keep your valuation defensible

“Defensible” is the word that matters in SIC. It means a judge can follow your logic, see your assumptions, and challenge them on their merits rather than guessing what you did. Three habits get you most of the way there. First, state every assumption out loud — growth rate, discount rate, peer set — so they can be inspected. Second, show a range, not a single number: a value of “$40–48, base case $44” is more honest and more credible than a false-precision “$43.71.” Third, cross-check your two methods: if your DCF says $44 and a peer multiple says $20, that gap is not a problem to hide — it is the most interesting thing in your pitch, and explaining it is where you win marks.

A practical reality check the professionals use: even if your main method is a DCF, run a quick multiple on your conclusion. It is often easier to spot an over-aggressive DCF by looking at the multiple it implies than by staring at the inputs. If your DCF implies the company should trade at 60× earnings while its peers trade at 15×, your growth assumptions are probably doing too much work. For more on turning these numbers into a written argument, see our walkthrough on building an SIC investment thesis.

The valuation mistakes judges spot first

When a valuation loses marks in SIC, it is usually one of a handful of recurring errors. Knowing them in advance is the cheapest way to raise your score.

- Confirmation bias. The single most common pitfall: deciding you like the stock first, then quietly lowering the discount rate or raising the growth rate until the math agrees. Judges are trained to look for inputs that are conveniently flattering.

- A terminal value that swallows the model. In a DCF, a terminal value of roughly 60–75% of total value is normal; one above ~85% is a red flag that nearly all your value rests on guesses far in the future.

- Mismatched multiples. Pairing enterprise value with net income, or equity value with EBITDA. The numerator and denominator must belong to the same group of investors.

- A lazy peer group. Calling any company in the same sector a “peer.” Good comparables share growth, margins and business model — not just an industry label.

- False precision. A target of “$43.71” implies a confidence no model deserves. A range with a clearly labelled base case reads as more sophisticated, not less.

- No “so what.” A value with no comparison to the current price is not a thesis. Always end with the gap: price is X, value is Y, here is why the market is wrong.

Notice that most of these are reasoning errors, not arithmetic errors — which is exactly why SIC weights clarity of thinking over the size of your spreadsheet. A useful test is to ask whether you would still believe your conclusion if a skeptic, not a fan, had built the model. If you want a structured way to pressure-test your work, our guide on how to prepare for SIC (self-study vs coaching) shows where outside feedback adds the most value.

A beginner’s order of operations

Putting it together, a sensible first valuation for an SIC pitch runs in this order: (1) understand the business well enough to know what drives its cash; (2) run a quick multiple to anchor yourself to the market; (3) build a simple 5-year DCF with assumptions you can defend; (4) compare the two and produce a value range; (5) state the gap to the current price as your thesis. Do that cleanly and you will already be ahead of most beginners, who skip straight to a complicated model and forget to say why anyone should care.

Frequently asked questions

Do I need a DCF to do well in SIC?

No. A clean multiples valuation with a clear thesis can score well. SIC rewards defensible reasoning, not the most complex model you can build.

What discount rate should a beginner use?

There is no single right number. State your assumption, justify it briefly, and test how your value changes if it moves a percentage point either way.

Is SIC the same as the Wharton investment competition?

No. SIC and the Wharton Global Youth High School Investment Competition are separate events run by different organisations. This site covers SIC.

Talk to an advisor

Have a valuation or thesis you want a second pair of eyes on before the season? Message us directly:

- 💬 WhatsApp — message an advisor directly → · fastest reply

- 📧 Email meiqiqiang@linstitute.net · 24-hour reply

Published by the SIC editorial desk, operated by Hanlin Education for China-based international-school students. The Student Investment Challenge (SIC) is a distinct competition from the Wharton Global Youth High School Investment Competition; the two are run by different organisations. This article is an educational primer and not investment advice; please confirm current rules, dates and formats on the official SIC site. We correct any errors within 7 working days.