Most teams that miss advancement in the Student Investment Challenge (SIC) do not lose on returns — they lose on craft. The four recurring mistakes are over-diversification (no real position), no defensible thesis, valuation hand-waving, and risk treated as an afterthought. Because SIC judges process on a four-axis rubric — thesis clarity, evidence quality, risk articulation, revision discipline — each of these maps to points you can recover before the deadline.

Why “good portfolio, weak report” loses

The single biggest misconception about SIC is that a green portfolio carries the entry. It does not. As the official program states, advancement turns on the clarity and articulation of the thesis, not on the growth of the portfolio. SIC is a CEE-endorsed research program for grades 6–12 with two tracks: the Junior Division (Trading Track), where each student runs a simulated portfolio and files a weekly thesis log, and the Senior Division (Strategy Track), where teams of two to four produce a single end-of-stage investment strategy report.

This matters because it changes what a “mistake” even is. A team can finish the season up double digits and still not advance if the reasoning behind those trades was never written down, defended, or revised. Conversely, a flat portfolio with a sharp, falsifiable thesis can read as stronger work. If you have not internalised this, every fix below will feel optional — and it is not. (For how SIC differs from the separate Wharton Global Youth High School Investment Competition, which ranks teams in a tournament, see our standalone comparison — the two reward different things.)

From the desk: across the entries we coach for China-based international-school students, the failure pattern is almost never ignorance of finance. It is students who can do the analysis but never make the report argue. The rest of this piece is about closing that gap.

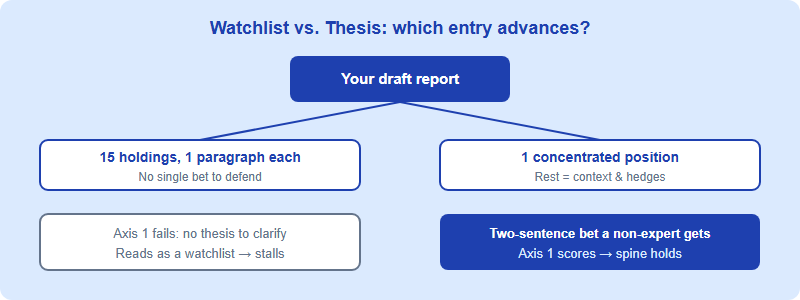

Mistake 1 — Over-diversification: owning everything, betting on nothing

The most common Senior-Division error is a report that covers a basket of 12–20 holdings, gives each a paragraph, and never commits to a single defended position. It feels safe and “balanced.” On the rubric it is the opposite of safe: a diffuse portfolio has no thesis to clarify, so Axis 1 (Thesis Clarity) collapses, and with it the spine of the whole report.

SIC’s Senior Division is explicit about scope — the deliverable is “a single end-of-stage investment strategy report: a defended thesis on one company, sector, or macro position.” That word one is doing real work. The rubric’s first axis asks: “Can a non-expert understand the bet in two sentences?” You cannot answer that for a 15-stock grab-bag.

The fix: pick one concentrated thesis (a single company, one sector view, or one macro position) and let the rest of the portfolio exist only as context or hedges around it. Write your two-sentence bet first, before any analysis. If you cannot state it in two sentences a non-expert understands, you do not yet have a thesis — you have a watchlist.

Mistake 2 — No thesis: a report that describes instead of argues

Even teams that pick one company often fail to make a claim. The report becomes a company profile: history, products, management bios, a revenue chart. All accurate, none of it an argument. The reader finishes the page and cannot say what you believe will happen, why, or by when. On Axis 1 this is fatal, and it quietly drags down Axis 3 too — you cannot articulate risk to a thesis that was never stated.

A thesis is a falsifiable claim with a direction and a reason: not “Company X is a strong business” but “X is mispriced because the market is treating its margin compression as structural when our channel evidence shows it is cyclical, and we expect re-rating as that becomes visible over the next two to four quarters.” Notice it can be wrong — that is the point, and it is exactly what Axis 3 (Risk Articulation) will test next.

The fix: draft the thesis sentence before you research the supporting case, then spend the report defending or revising it. A useful self-test from our editing desk: highlight every sentence in your report that an encyclopaedia could also have written. If 80% of the page survives that highlighter, you have written a description, not a thesis. Our breakdown of the SIC four-axis rubric walks through what a thesis-led paragraph looks like in practice.

Mistake 3 — Valuation hand-waving: “undervalued” with no number

The third recurring mistake is asserting a valuation conclusion without showing the work. Reports say a stock is “undervalued,” “trading at a discount,” or “has significant upside,” and then stop. There is no multiple, no comparison set, no scenario, no stated assumption a reader could disagree with. This is an Axis 2 (Evidence Quality) failure: the rubric explicitly rewards primary sources — 10-Ks, earnings transcripts, Fed minutes — and penalises secondary aggregators and unsupported summaries.

You do not need a 40-tab discounted-cash-flow model to satisfy this. You need traceable reasoning. A simple, defensible comparable-multiples table with the source of each input beats an elaborate DCF whose assumptions are invisible. The judge’s standard, per the rubric, is whether a number can be traced to its primary source in under thirty seconds.

| Valuation claim | Hand-waving version (weak) | Defensible version (Axis 2 ready) |

|---|---|---|

| Headline | “The stock is clearly undervalued.” | “At 11× forward earnings vs. a 16× five-year peer median, the market is pricing permanent decline.” |

| Source | None / a finance blog | Multiple from the latest 10-K and earnings transcript; peer set named |

| Assumption | Implicit, unstated | “Assumes margins recover to the FY23 level; if they don’t, fair value is ~20% lower.” |

| Scenario | Single rosy outcome | Bear / base / bull with one driver each |

| What a judge sees | An opinion | A number they can check and argue with in 30 seconds |

The fix: for every valuation adjective (“cheap,” “expensive,” “upside”), force yourself to attach one number and one primary source. If you cannot, cut the adjective. A report with three numbers you can defend is stronger than one with twenty you cannot.

Mistake 4 — Ignoring risk (and never revising)

The last two axes — Risk Articulation and Revision Discipline — are where strong-on-paper teams most often leave points on the table, because both feel like admitting weakness. They are the opposite. Axis 3 asks a single question: “What would have to be true for this thesis to be wrong?” A generic line like “macro conditions could affect the stock” earns nothing. The rubric rewards concrete, falsifiable terms — specific metrics, thresholds, and timeframes.

Axis 4 (Revision Discipline) is the one most teams forget exists. It evaluates whether you updated your view as facts changed — and explicitly penalises retrofitting analysis to match portfolio performance after the fact. For Junior-Division students, this is precisely why the weekly thesis log matters: it is your timestamped evidence that you reasoned in real time, not in hindsight. A clean log that shows a position changed and why is worth more than a log that pretends you were right all along.

The fix: end your report (or each weekly log) with an explicit “What would prove us wrong” section — two or three falsifiers stated as metrics with thresholds and dates (“if same-store sales fall below +2% for two consecutive quarters, the cyclical-recovery thesis breaks”). Then, if the facts move, revise in writing and say what changed. Judges reward the update; they penalise the cover-up.

A pre-submission checklist (run it the week before)

None of these fixes require more finance knowledge — only more discipline in how the thinking is written down. Before you submit, run this against the official four-axis standard:

- Thesis (Axis 1): Can a classmate outside finance restate your bet in two sentences after one read? If not, rewrite the opening.

- Evidence (Axis 2): Can every key number be traced to a 10-K, transcript, or primary filing in under 30 seconds? Delete what can’t.

- Risk (Axis 3): Do you name at least two concrete, dated, measurable falsifiers? “Macro risk” does not count.

- Revision (Axis 4): Does your report or log show at least one place you updated your view as facts changed — and why?

- Scope: Is the report a defended thesis on one company, sector, or macro position — not a basket?

- Process facts: Have you confirmed your division, eligibility (grades 6–12; Senior teams of 2–4; school consent for grades 6–9), and the current submission window on the official SIC site? Deadlines and timezone should be confirmed there — 以官方为准.

SIC registration is handled through a real program staff member via the official intake (there is no public online form), so use that channel to confirm anything procedural rather than assuming it works like another competition.

FAQ

Does a high-return portfolio guarantee I advance in SIC?

No. SIC states advancement turns on the clarity and articulation of the thesis, not portfolio growth. A defended, falsifiable argument outweighs a green return.

What’s the single most common mistake judges see?

Over-diversification with no defended position. The Senior report should be one thesis on one company, sector, or macro call — not a 15-stock summary.

How do I avoid losing points on the valuation section?

Attach one number and one primary source (10-K, transcript) to every valuation claim. The rubric rewards traceable evidence, not adjectives like “undervalued.”

Is SIC the same as the Wharton high-school competition?

No — they are separate programs run by different organisations. SIC is rubric-judged research; Wharton is a ranked tournament. They reward different qualities.

Published by the SIC editorial desk, operated by Hanlin Education for China-based international-school students. SIC is distinct from the Wharton Global Youth High School Investment Competition (a different entity). Official rules are set by the competition and change yearly, so always confirm current details — registration, eligibility, deadlines, timezone, and judging — on the official SIC / organiser site. Confirmed errors corrected within 7 working days.